The current Real Estate market in Long Beach continues to be strong. However the climb back to 2006’s peak values from 2011’s bottom, may be running up against a little bit of resistance as this year unfolds. My outlook is positive, but there are concerns on the horizon.

The current Real Estate market in Long Beach continues to be strong. However the climb back to 2006’s peak values from 2011’s bottom, may be running up against a little bit of resistance as this year unfolds. My outlook is positive, but there are concerns on the horizon.

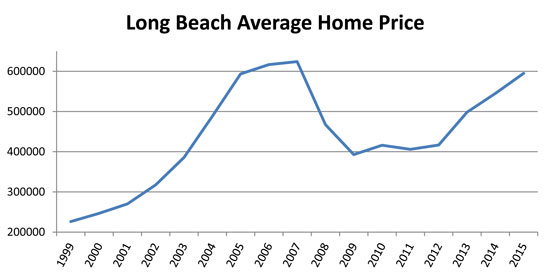

The History of Long Beach Home Prices

The graph below shows home values are returning to peak 2006 values. Does this mean the market is then becoming over-priced? Absolutely not. In fact at today’s rates homes are VERY fairly priced.

Since 2006’s peak value, almost 10 years have elapsed. During this time, incomes went up and rates went down. If a buyer’s income increased by 2% per year, their income would be 24% greater today (compounding included). Plus, in 2006, rates were around 6.5% versus today’s low 4%, resulting in a massive 27% drop in a buyers mortgage payment. Lower rates have been a huge tailwind in assisting the recovery.

Prior to 2006’s peak, the previous peak in prices was 1990. Prices didn’t surpass 1990’s values until 1998. Another important observation is that once the previous 1990 peak was hit in 1998, home prices continued to take off.

Arguments for a Continued Rally

Values are at Fair Market Relative to Rent

In 2006 I noted that homes were wildly overvalued by 40% relative to rent. This check and balance is the comparison between a homes total payment and it’s fair market rent.

Today the average home in East Long Beach sells for around $585,000. This home is a 3 bedroom 1.75 bath with around 1,500sf and rents for around $2,400 to $2,500. With 10% down and a 30 year mortgage at 4%, the total payment would be $3,222 (including property taxes and insurance). Homeowners receive significant tax benefits. Mortgage interest and property taxes deductions results in significant tax savings. For this reason my formula takes only 75% of the home payment of $3,222 and compares it to rent, for which there are no tax deductions. This results in a rental equivalent home payment of only $2,417 ($3,222 x 75%). Right in line with fair market rent.

Buying an average home in East Long Beach with 10% down is then essentially equivalent to renting the same home. This is BIG because this comparison usually shows a home purchase to be a slight financial premium versus renting.

This comparison (mortgage vs. rent) had home prices 25% and 40% overvalued during the 1990 and 2006 peaks respectively. Undervaluations were only about 10% during the market bottoms of 1995 and 2011, and this undervaluation was very brief. This comparison usually shows homes as slightly overvalued, which means that most times buyers will pay a slight premium to own a home. I believe it is reasonable for homes to show as slightly overvalued relative to rent, as I believe home ownership has more financial advantages than renting.

The fact that homes currently show fair value relative to rent is a big stabilizing factor and reduces the potential of a future market decline and actually bodes well for future appreciation. But note that mortgage payments change 10% with every 1% change in mortgage rates. While the market has been the beneficiary of lower rates over the last 3 decades, the market may suffer if rates go higher.

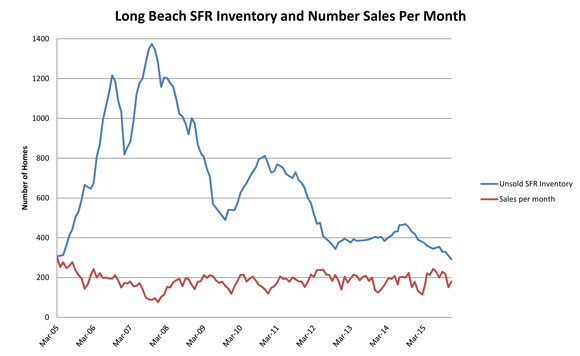

Inventory Tightens

Probably the single best future indicator that I have tracked since 1990’s correction, has been the ratio of inventory versus sales or “Number of Month’s Supply.” This is extremely valuable because this indicator is predictive. Most indicators just report on the past.

When the market turned in 1990 it was common to have 10 homes on the market for every home that sold within a 30 day period. When the market turned down after the credit crunch of 2007, there were once again 10 or more homes on the market for every one that would sell within 30 days. The predictive value can be seen when you ask these questions. As a homeowner, “If only 1 of 10 homes sells every month, and if my home is priced like the other homes I am competing with then my home has only a 1 in 10 chance of selling in the next 30 days?”. Not very good odds. If you want to increase your odds of selling when competing against 10 other homes, you need to lower your list price and make it more attractive. It would be reasonable to expect that you would have undercut your competition and be either the best home on the market or at least in the top few, to attract that one buyer.

Where we stand today, a low inventory sellers market, is the complete opposite of a high inventory buyers market. This has only become more apparent as inventory has continued to drop through all of 2015. Sales of homes in Long Beach have averaged a little less than 200 per month for the last several years. With only 300 homes on the market, this provides only a 45 day supply of homes, so there are not many homes to choose from, which has shortened the days homes are on market when homes are priced well.

So if the housing market was in a bubble, there would be nothing to worry about, but outside forces are significant.

Properties are Currently Held by Strong Hands

The last run up in prices from 2000-2006 saw loans approved to anybody that could fog a glass. After the credit crunch of 2007 caution has been the rule of the day. Underwriting guidelines and standards have been quite conservative and rigid, meaning buyers that qualify for their home mortgages can actually make the payment. This will give the housing market solid footing moving forward. Only if the economy goes into a severe recession and puts jobs at risk will this change.

Arguments Against a Continued Rally

The Fed is Out of Ammo

Recently on CNBC (January 6th, 2016), former Dallas Fed head Richard Fisher stated, “We Front loaded a Tremendous Market Rally” and Warns “No Ammo Left”.

During a 5 minute confessional interview, while talking heads attempt to blame China (and now North Korea) for recent US market volatility, Fisher explains “Its not China,” it is The Fed that is at fault: “What the Fed did, and I was part of it, was front-loaded an enormous rally, in order to create a wealth effect… and an uncomfortable digestive period is likely now” Simply put, Fisher concludes there can’t be much more accommodation, “The Fed is a giant weapon that has no ammunition left”. It is fair to say that the Fed achieved their goal, rising asset prices.

The “Wealth Effect” is a change in spending that accompanies a change in ones perceived wealth. When stock portfolios or home prices rise, people tend to spend some of those gains, and lend a boost to the rest of the economy. This also happens in reverse.

Easy money policies, however, eventually need to be reversed. While quantitative easing has been deemed by some to be a success, any declaration of victory must be withheld until rates are brought back to market values and the huge run up in the Feds balance sheet is reduced. The economy has to be resilient enough to withstand the unwinding of quantitative easing and the likely higher rates that may accompany before victory can be declared. This has not happened yet, so a declared victory is premature.

As I had previously mentioned the big drop from 2006’s interest rates of 6.5% to 2015’s current interest rates of 4% resulted in a 27% drop a buyers payment. While 4% is not zero, the corresponding Fed funds overnight rates are essentially zero, and the Federal Reserves business model of lowering rates or printing money to goose the economy may have run its limit, so says former Fed Official Richard Fisher.

At what point might this tailwind become a head wind? Obviously this is more of a rhetorical question as I do not have the answer. It does however point to an issue of instability in our economy as a result of debt levels being too high. This is just too big of a question to handle within the scope of a newsletter. In addition, there really is no precedent to the situation we have on hand. Is this first week of trading after the Feds cautious 1/4 pt increase, the first within nearly 10 years, any indication?

The Stock Market is Floundering

As I write this article we just finished the first two weeks of trading. The financial news has reported that this is the worst first week of trading (on a percentage basis) ever! There is a saying that as the first week goes, so goes the month and so goes the year. Is this nervousness from North Korea’s nuclear test, or from China’s market melt down? Richard Fisher says no.

So former Fed official Richard Fisher says we may have some pain ahead. But from my observations, there may not be many places to hide, and Real Estate may be a safer bet that others. It is likely that if there is a large financial correction, Real Estate would take some type of hit, but at least Real Estate is something real, and in the case of income producing property there is a definite yield. A real yield has become something to be coveted. In the grand scheme of investments, return on investment (ROI), is everything. Only when losing your capital becomes a real concern does ROI become secondary. As the saying goes, the only thing that is more important than ROI, is the return of your capital. With most countries creating lots of liquidity through their printing presses, the value of holding cash as the safest alternative may be called into question.

Real Estate – A Place to Park Your Cash?

This leads me to a quick anecdotal Real Estate story. My sister recently sold her brownstone in Brooklyn. When she purchased the property she consulted with me as she was nervous about the purchase price of $330,000 and wanted to make sure it was smart move. At around the same time, 1997, I had just purchased a home which for approximately $250,000. Since then my investment slightly more than tripled to a little more than $750,000. If here brownstone when up similarly then it would be worth around 1 million, but the value soared well beyond.

For more than a decade, my sister and husband had been living in London and Hong Kong, and were not planning on moving back to New York. My sister and brother-in-law did call me up to consult prior to the sale. What they said somewhat shocked me; they were told by the agent that helped them purchase the property that it might be worth 4 million. Since they were not returning to live in the property, theirs was a simple financial decision whether to keep the property or sell. I asked “What does the property rent for?”, “About 10k a month” was his reply. Ok then, as a general rule a landlord nets about 60% of the gross rents after, management, vacancy, taxes, insurance and maintenance. So their net annual rent would be $72,000 ($10,000 x 60% x 12). If the property is worth 4 million then the asset is returning 1.8% on your equity. My question to my brother-in-law, “Can you earn more on your money than 1.8%, while still preserving and /or growing your capital base”, if so then selling the property and investing the proceeds makes sense”. They sold the building, but the story is not over. The home was overbid by 1 million dollars, selling for 5 million all cash. At 5 million the property would have generated less than a 1.5% return.

What is my take away? That cash could be trash, and that investors are just looking for a place to park their assets. And maybe even a crappy 1.5% return on your money is better than keeping the money in the bank. While this is certainly an exciting story for my sister, it does make a statement that the investment landscape is not exactly ripe with fruitful high yield opportunities.

Property Values Rising – But Incomes are Sinking

David Stockman director of the Office of Management and Budget under Reagan notes on his website that home prices in major western cities are climbing, while median family incomes are declining. This is not a good sign. Should this continue, it will bring an end to the rise in home prices. A rise in home prices needs to be supported by rising incomes. As a side note, while cities are experiencing declining median family incomes, Washington D.C. is an exception. Hmmm…. not a good statement about the growth of government.

http://davidstockmanscontracorner.com/what-the-fed-or-foxcnbc-wont-tell-you-about-west-coast-home-prices/

Conclusion

In review, the housing market by itself is stable, fairly priced, or even very attractively priced, and low inventory predicts future price increases. However, the housing market floats in the sea of our economy, and the calmness of these waters is not certain.

What the Federal Reserve, along with many central banks, have done with excess liquidity has achieved its goal of re-inflating an alleged fragile financial system. How this unwinds is anybody’s guess because we are in uncharted waters.

Here are three ways this may unfold. The first is the loss of faith in paper currency. In this case Real Estate will be a good place to be. The second is the Government exits quietly through inflation. In this case Real Estate will be a good place to be. The third, and the honest way, would be for the Fed to reduce our debt on the balance sheet and allow rates to rise. This is not likely to happen as there will be some initial economic pain. This will initially be bad for Real Estate, as higher rates will make home payments go up. Each one percent increase in interest rates affects a mortgage payment by about %10. This will immediately affect a new borrower or a home owner looking to sell. The buyer that has locked in a 30 year fixed rate loan with no plans on selling should not be concerned. And after an initial price shock, home prices will stabilize.

The Federal Reserve has de-incentivized savers and encouraged speculation resulting in increased asset values. The result has been that investments with a good return have become hard to find. While Real Estate is no exception, it may be a better bet than other alternatives. In the case of a severe financial shock, Real Estate may be a better place to hide than most.